Finding Hidden Opportunities in Customer Purchasing Behavior.

This project uses Python-driven exploratory data analysis to uncover where sales can be improved. By examining customer behavior, unit volumes, and price sensitivity across segments, it highlights clear opportunities for growth and sets the foundation for later experimentation. This case study is based on two datasets, including one years worth of chips transaction data from 2018-07-01 to 2019-07-01, and customers overall grocery shopping behavior.

Where the Opportunity Lies

Out of the three customer segments, Mainstream shoppers, particularly young singles and couples, show the greatest opportunity to improve chip sales. Their purchasing patterns indicate clear areas for improvement.

These segments are derived from customers overall grocery shopping behaviors, beyond chip purchases.

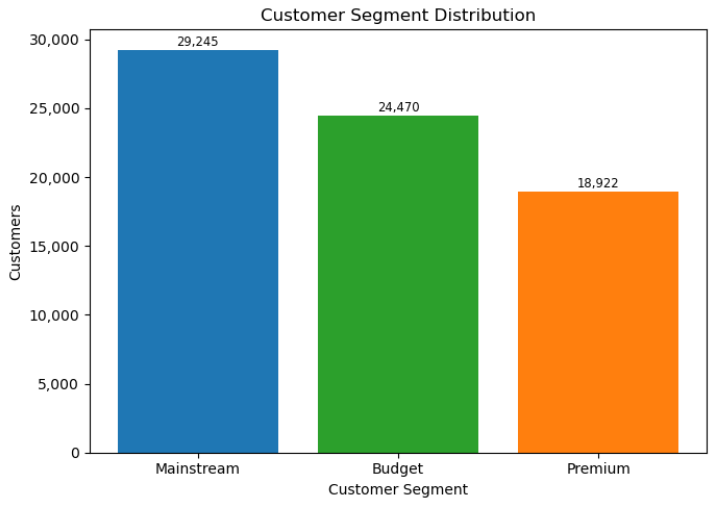

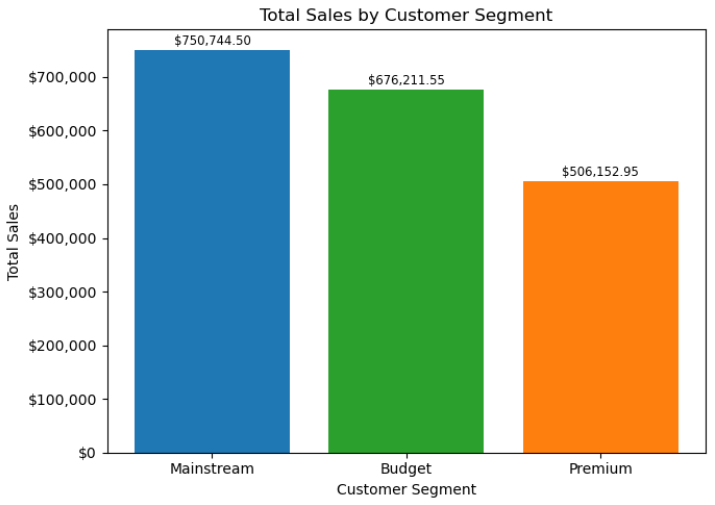

Contribution by Age Group

While the contribution from the Mainstream young singles and couples is already strong, 11.1% of all customers and 8.2% of all total sales, there’s definitely room for improvement. Despite being the biggest segment by a large margin, we see them falling behind Older families in terms of sales, suggesting that this group visits often but tend to spend less.

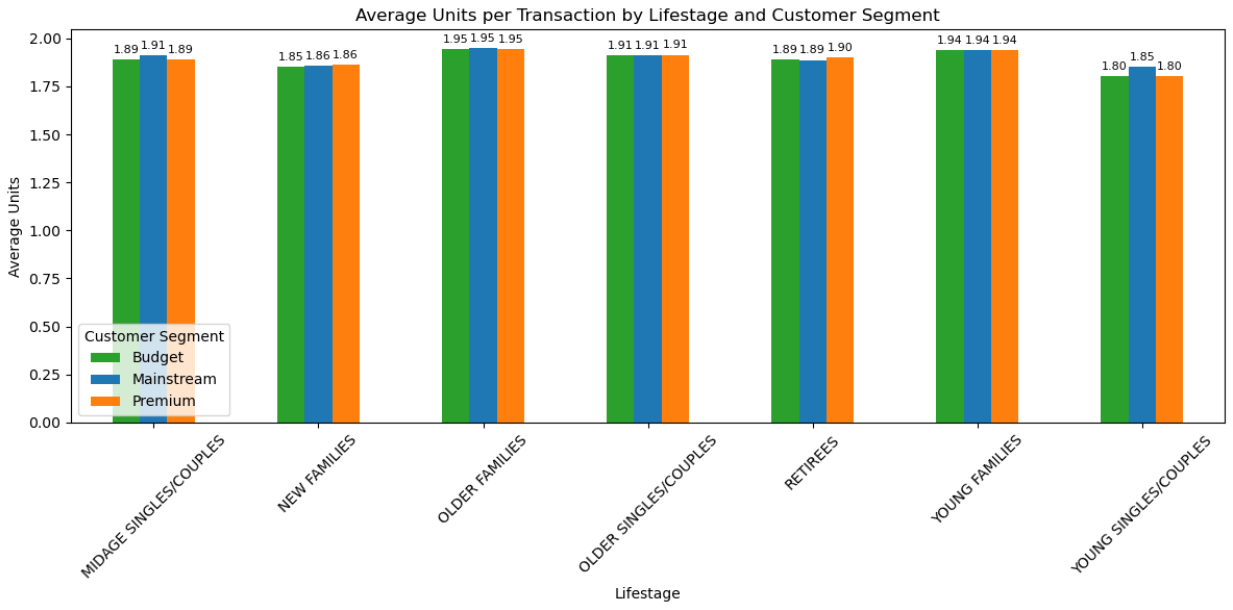

Customer Purchase Behavior

Customers generally buy similar quantities per trip, but Older and Young Families stand out for purchasing more units, which is expected and helps drive their higher sales contribution. Young Singles/Couples buy fewer units, lowering their total spend.

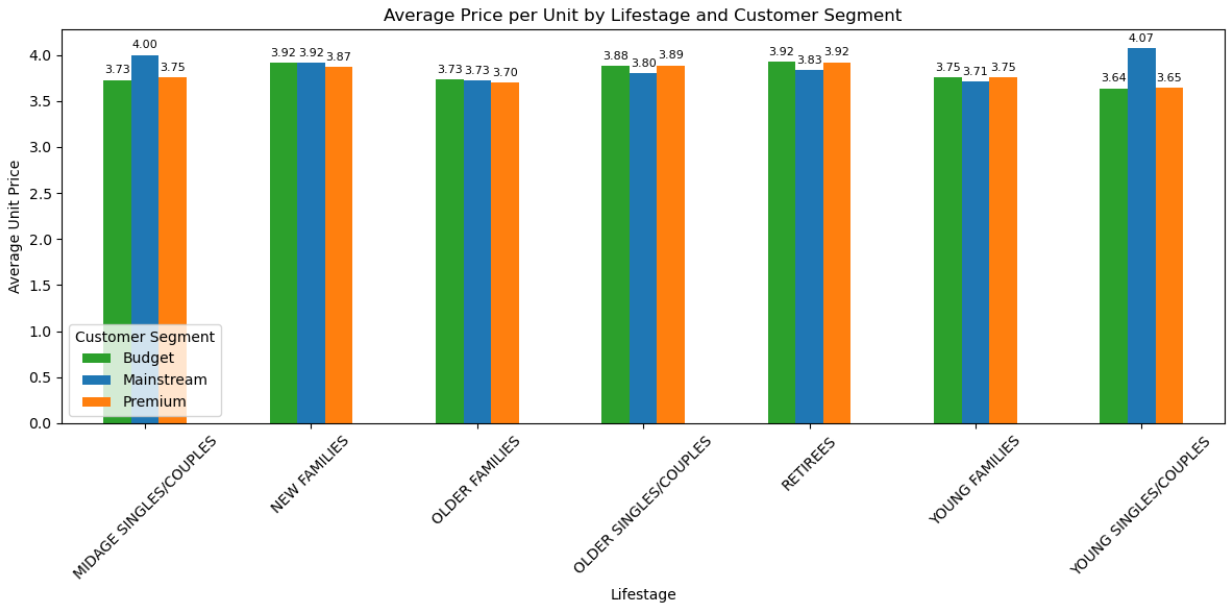

However, when looking at price per unit, Mainstream Young Singles/Couples and Midage Singles/Couples emerge as the least price-sensitive segments, consistently paying the highest prices by a significant margin. Meanwhile, Older Families, despite higher basket sizes, favor lower-priced products.

A t-test confirmed that this higher average price per unit among Mainstream Young and Midage Singles/Couples is highly significant (p < 2.2e-16), meaning they reliably pay more per unit than other segments.

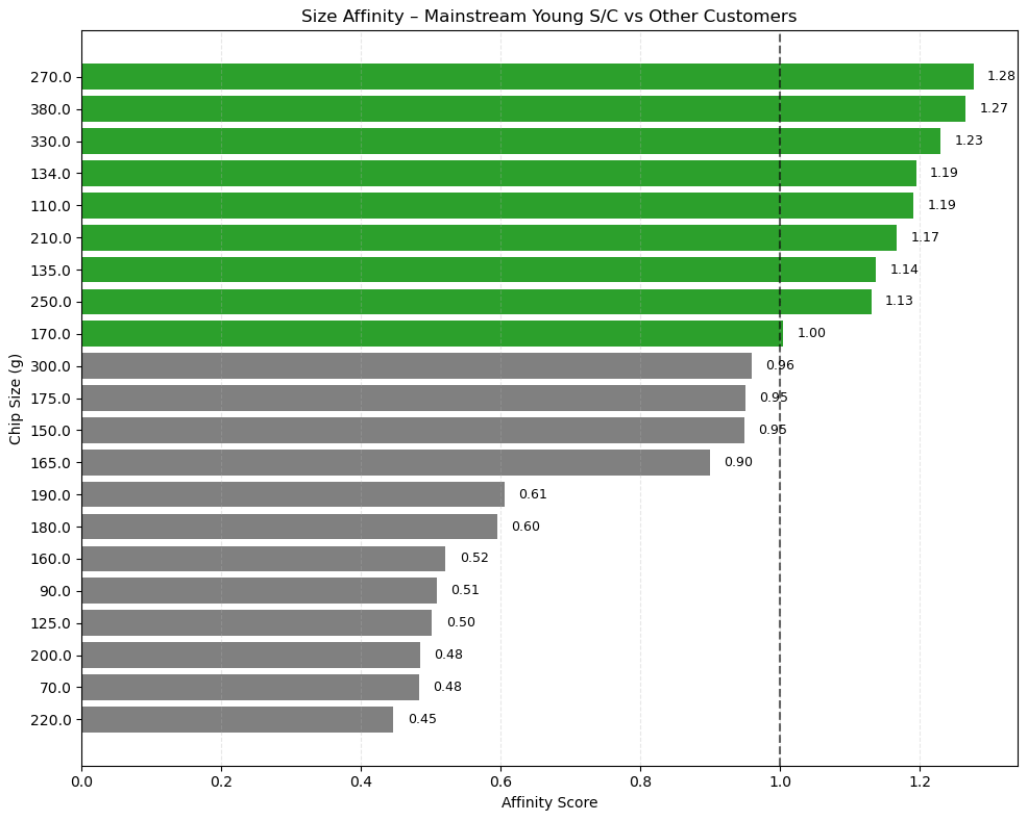

Target Segment’s Preference

Affinity scores above 1 suggests higher likelihood of purchase by Mainstream Young Singles/Couples (Ex. 1.24 = 24% more likely)

Mainstream Young Singles & Couples are significantly more likely to purchase Tyrrells, Twisties, and Kettle compared to other customers, indicating strong brand preferences that can guide targeted promotions and product placement.

Chip sizes around 270g, 380g, and 330g are more preferred by Mainstream Young Singles & Couples compared to other cusy, showing clear demand for mid-to-large bag formats that can be prioritized in merchandising and multi-buy offers.

Conclusion and Recommendation

Mainstream Young Singles & Couples are willing to pay more per unit, but purchases the fewest units per trip. This presents a strong opportunity to drive growth by boosting basket size, rather than increasing price. Small multi-buy incentives and improved visibility of their preferred brands and size could meaningfully lift sales. Maintaining premium product availability is also key, as their value is driven by willingness to pay.

Jupyter Notebook

Feedback

Anonymous feedback is welcome. All fields except the message are optional.